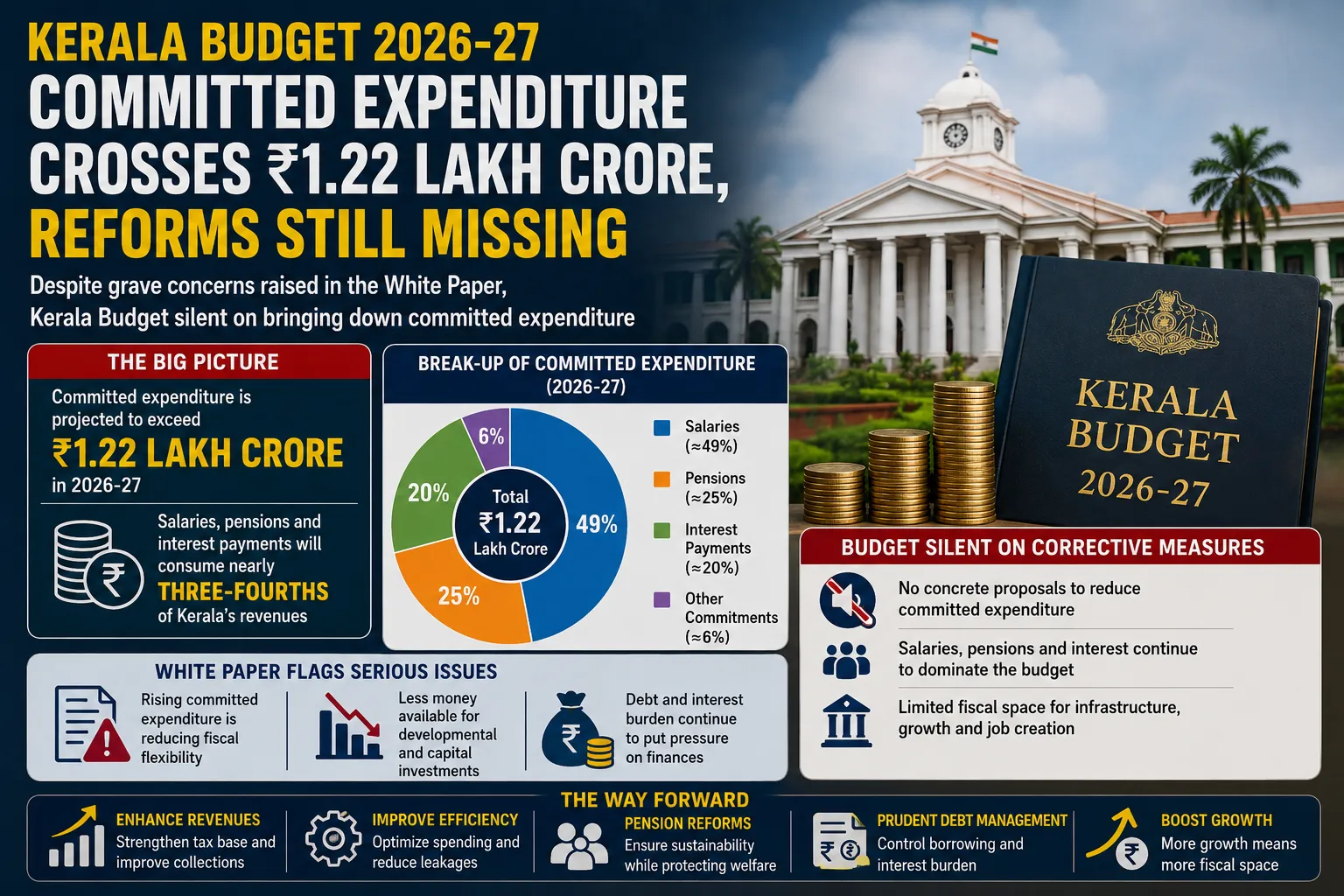

Kerala’s financial health has once again become the subject of intense debate following the presentation of the State Budget for 2026-27. Despite serious concerns highlighted in the state’s White Paper on public finances, the Budget has remained largely silent on introducing concrete measures to reduce the rapidly rising burden of committed expenditure.

According to budget estimates, Kerala’s committed expenditure—which includes salaries, pensions, and interest payments—is projected to exceed ₹1.22 lakh crore during the 2026-27 financial year. This amount is expected to consume nearly three-fourths of the state’s own revenue receipts, leaving limited fiscal space for developmental activities and capital investments.

The situation has renewed discussions among economists, policymakers, and financial experts regarding the sustainability of Kerala’s fiscal model and the urgent need for structural reforms to maintain long-term financial stability.

Understanding Committed Expenditure

Committed expenditure refers to mandatory government spending that cannot easily be reduced in the short term. These expenditures generally include:

-

Salaries and allowances of government employees

-

Pension payments to retired employees

-

Interest payments on outstanding debt

-

Other legally binding financial obligations

Unlike discretionary spending, committed expenditure is unavoidable because it arises from contractual, legal, or administrative commitments already made by the government.

While such expenditure is essential for maintaining government functions and meeting obligations toward employees and creditors, excessive growth in these liabilities can significantly constrain a government’s ability to invest in development projects and public services.

Kerala’s Fiscal Position Under Pressure

Kerala has traditionally maintained one of the country’s strongest social development indicators, performing exceptionally well in education, healthcare, and human development. However, achieving these outcomes has also required substantial public expenditure over several decades.

The state’s fiscal pressures have gradually intensified due to several factors, including:

-

Increasing salary commitments

-

Growing pension liabilities

-

Rising debt servicing obligations

-

Higher social welfare spending

-

Repeated natural disasters and emergency expenditures

-

Economic disruptions caused by the pandemic

As a result, committed expenditure has steadily increased and now constitutes a dominant share of Kerala’s annual budget.

The projected figure of more than ₹1.22 lakh crore in 2026-27 highlights the magnitude of the challenge.

Salaries Continue to Form a Major Component

A significant portion of Kerala’s committed expenditure consists of salaries paid to government employees.

Kerala has one of India’s largest public service systems relative to its population size. The state operates an extensive network of schools, hospitals, local self-governments, and administrative institutions that require substantial staffing.

Periodic pay revisions, dearness allowance increases, and recruitment requirements naturally contribute to rising salary expenses.

Government employees play a critical role in delivering public services, and salary expenditure represents an investment in administrative capacity. However, when salary obligations consume a large share of revenues, governments may struggle to allocate sufficient funds for infrastructure development and new policy initiatives.

Pension Liabilities Are Increasing

Pension payments represent another significant component of Kerala’s fiscal burden.

As a large number of government employees retire each year, pension obligations continue to increase. Improvements in life expectancy have also resulted in longer post-retirement payment periods.

Pension expenditure is particularly challenging because it is largely non-discretionary. Governments cannot simply reduce pension payments without affecting legal obligations and social security commitments made to retired employees.

Many states across India are experiencing similar concerns, but Kerala’s demographic profile and historical public employment patterns have made pension liabilities especially significant.

Financial experts have repeatedly emphasized the importance of developing sustainable pension systems capable of balancing employee welfare with long-term fiscal stability.

Rising Interest Payments Add to the Burden

Interest payments on accumulated debt constitute the third major component of Kerala’s committed expenditure.

Like most states, Kerala relies on borrowing to finance capital projects and bridge fiscal gaps. Borrowing itself is not inherently problematic if it finances productive investments that generate economic growth.

However, increasing debt levels eventually result in higher interest obligations.

As debt servicing requirements grow, a larger share of annual revenues is diverted toward paying interest instead of funding development activities.

This phenomenon can create a cycle in which governments borrow additional funds simply to manage existing liabilities, further increasing long-term fiscal pressure.

The White Paper had reportedly highlighted concerns regarding this growing debt burden and its implications for fiscal sustainability.

White Paper Raised Serious Concerns

The White Paper on Kerala’s finances presented a sobering assessment of the state’s fiscal condition.

The document reportedly acknowledged that committed expenditure was expanding rapidly and reducing the government’s flexibility in managing public finances.

One of the central concerns highlighted was that mandatory spending obligations were consuming an increasingly larger proportion of available revenues.

When most revenues are allocated toward salaries, pensions, and interest payments, governments have limited resources available for:

-

Infrastructure projects

-

Industrial development initiatives

-

Social sector expansion

-

Public transport improvements

-

Digital transformation programs

-

Climate resilience projects

The White Paper therefore underscored the importance of implementing structural reforms to improve fiscal sustainability.

Budget Remains Silent on Corrective Measures

Despite these concerns, observers have noted that the 2026-27 Budget contains few concrete proposals specifically aimed at reducing committed expenditure.

The absence of detailed corrective strategies has prompted criticism from some economists and fiscal analysts.

While the Budget outlines developmental priorities and social welfare initiatives, it provides limited information regarding long-term plans to manage the state’s rising mandatory expenditure commitments.

Fiscal experts generally agree that reducing committed expenditure is not a simple process.

Salary and pension obligations involve employees and retirees whose livelihoods depend upon these payments. Similarly, interest payments represent legal commitments that must be honored.

Nevertheless, many economists argue that governments should establish gradual reform pathways rather than postponing difficult decisions indefinitely.

Development Spending Faces Constraints

One of the most significant consequences of high committed expenditure is the reduction in fiscal space for developmental expenditure.

Capital investment plays a vital role in generating economic growth. Investments in roads, ports, industrial corridors, healthcare infrastructure, and education facilities create employment opportunities and improve long-term productivity.

When mandatory spending consumes most available revenues, governments often have fewer resources for such investments.

This can affect future economic growth potential and limit opportunities for private investment.

For a state like Kerala, which aims to attract investment and generate employment opportunities for its highly educated workforce, maintaining adequate capital expenditure remains particularly important.

The Need for Structural Reforms

Addressing committed expenditure requires long-term strategic planning rather than short-term solutions.

Experts often recommend a combination of measures, including:

Revenue Enhancement

Strengthening tax administration and expanding revenue-generating activities can improve fiscal capacity.

Efficient Public Spending

Improving administrative efficiency may help optimize government expenditure without compromising public services.

Pension Reforms

Sustainable pension mechanisms can reduce long-term liabilities while protecting employee welfare.

Debt Management

Prudent borrowing strategies and improved debt management practices can help moderate interest obligations.

Economic Growth Initiatives

Higher economic growth generally expands the revenue base, making it easier to manage committed expenditure over time.

Implementing these reforms requires careful planning, political consensus, and administrative commitment.

Balancing Welfare and Fiscal Discipline

Kerala’s situation illustrates one of the central challenges in public finance management: balancing social commitments with fiscal sustainability.

The state has built an impressive record in human development through extensive public investment in education, healthcare, and social welfare. These achievements have significantly contributed to Kerala’s high quality of life indicators.

At the same time, maintaining these accomplishments requires a financially sustainable framework.

Fiscal discipline does not necessarily imply reducing welfare spending. Rather, it involves ensuring that public finances remain capable of supporting developmental goals over the long term.

Looking Ahead

The projected committed expenditure of over ₹1.22 lakh crore in 2026-27 serves as an important reminder that Kerala faces increasingly complex fiscal challenges.

As mandatory spending obligations continue to rise, policymakers may need to initiate deeper discussions regarding expenditure reforms, revenue enhancement strategies, and sustainable debt management practices.

The state’s future fiscal stability will likely depend on its ability to preserve social development achievements while creating sufficient fiscal space for economic growth and infrastructure investment.

Conclusion

Kerala’s Budget for 2026-27 has reignited concerns about the state’s growing committed expenditure burden. With salaries, pensions, and interest payments projected to exceed ₹1.22 lakh crore and consume nearly three-fourths of state revenues, fiscal flexibility is becoming increasingly limited.

Although the White Paper acknowledged the seriousness of these challenges, the Budget offers limited details regarding specific measures to address them. As Kerala seeks to sustain its impressive social development record while promoting economic growth, managing committed expenditure will remain one of the state’s most critical policy challenges.

The path forward will require thoughtful reforms, prudent financial management, and a long-term strategy that balances fiscal responsibility with social and developmental priorities.

roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel roystonhotel